概念

1. 社會投資回報(SROI)是甚麽?

2. SROI分析在項目管理上能發揮甚麽功能?

3. 有進行SROI研究的指引嗎?

「六階段分析模型」由英國政府内閣辦公室轄下的第三部門辦事處發佈,是國際上其中一個最常用的SROI研究方法。 [8] SROI研究的六個階段分別爲

(1) 確定研究範圍與影響所及的持份者,

(2) 辨識項目創造的成果,

(3) 印證成果並以數值標籤,

(4) 將成果換算爲社會效益,

(5) 計算SROI, 以及

(6) 報告和應用SROI計算結果.

六階段模型的詳情可參閱 這裏.

除此之外,研究人員亦提出了其他設計和執行SROI研究時的考慮因素。例如英國内閣辦公室轄下第三部門辦事處的指引提倡了SROI研究的七個原則(請參閲報告的96-98頁)。美國的學術研究機構發佈了SROI研究的十項指引(請參閲指引的120頁)。

本地亦有不少和SROI研究相關的參考資料,例如Social Impact Measurement – Workbook: A step-by-step approach to devising outcome indicators和Introduction to Social Impact Measurement Hong Kong Context提供了在香港社會環境下進行SROI研究的參考指引。賽馬會「衡坊」培訓計劃 (請參閲版面 成效/影響指標資料庫)和社會影響研究中心(請參閲 下載)亦提供了實用的SROI研究資源(例如常用社會成果的量度指標)。

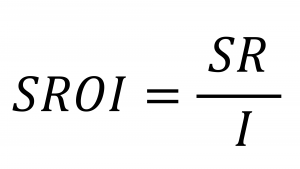

4. 如何估算項目的SROI?

SR 代表項目或服務在特定時間内的貨幣化社會價值,而 I 則代表在同段時間投入到項目或服務的投資額(例如資助)。另外,一般的計算方法都會將 I 和 SR 折現,以現時價值(present value)表達,而折現率根據某地方的平均通脹率而定。

在計算 SR 時,其中一個重要考慮因素是增益性(additionality),即能歸因於項目的社會回報。 [9] 當中的理由是如果某社會成果在沒有項目的情況下仍存在,將它歸因於項目是不合理的。

增益性的考量一般會涵蓋四個關鍵概念:淨損失因子、替代因子、歸因因子、以及遞減因子。A guide to Social Return on Investment有詳細的闡釋。

淨損失因子(deadweight):量度沒有任何項目下仍會存在的社會成果

替代因子(displacement):量度項目置換的其他社會成果

歸因因子(attribution):量度歸因於其他項目的社會回報

遞減因子(drop-off):隨時間變化的社會回報(例如減少)

進行計算時以上四個概念均以%表達。

5. 如何將社會價值貨幣化?

將社會成果貨幣化即是計算者將貨幣價值,亦即財務代理變數 (Financial Proxy),估算社會成果。一般來説,將社會價值貨幣化的方式有兩種。 [10] 兩種方式分別是“社會機會成本“(SOC) ,以及“願付價格” (WTP) 。

社會機會成本

社會機會成本是“在進行某種活動是所付出的稀有資源的價值“ 或 ”社會節省了的資源的價值”. [11] 在這裏,財務代理變數被理解為項目為受惠者創造社會價值時放棄了的社會機會成本,或在過程中社會節省了的機會成本。一般的計算方法會以財政或市場數據作“財務代理變數”。 [12]

例子:

|

項目 |

目標 |

社會成果 |

財務代理變數 |

貨幣化原理 |

|

康復更生計劃 |

協助更生人士重新融入社會 |

提升自尊 改善心理健康 |

每位受惠者的單位成本 |

項目在創造社會價值時放棄了的社會機會成本(稀有資源) |

願付價格

至於在願付價格的方式,社會成果的財務代理變數則被理解為市民平均願意支付給物品或服務的金額。 [13] 這種方式是由補償剩餘和相等剩餘等福利經濟學概念引申出來,計算每人平均願意接受或放棄多少來換取福祉上的得益。 [14]

例子:

|

項目 |

目標 |

社會成果 |

財務代理變數 |

貨幣化原理 |

|

改善醫療保健服務的項目 |

改善受惠者(例如長者)的健康狀況 |

改善自評健康狀態 |

自評健康的願付價格 |

市民願意為相若程度的自評健康改善支付的平均金額 |

6. 如何解讀SROI?

1. Peter Scholten, Social return on investment: A guide to SROI analysis (Amstelveen, The Netherlands: Lenthe Publishers, 2006).

2. Ross Millar and Kelly Hall, “Social return on investment (SROI) and performance measurement: The opportunities and barriers for social enterprises in health and social care,” Public Management Review 15, no. 6 (2013).

3. Malin Arvidson et al., “Valuing the social? The nature and controversies of measuring social return on investment (SROI),” Voluntary sector review 4, no. 1 (2013).

4. Jed Emerson, Jay Wachowicz, and Suzi Chun, “Social return on investment: Exploring aspects of value creation in the nonprofit sector,” The Box Set: Social Purpose Enterprises and Venture Philanthropy in the New Millennium 2 (2000).

5. Florentine Maier et al., “SROI as a method for evaluation research: Understanding merits and limitations,” VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations 26, no. 5 (2015); Arvidson et al., “Valuing the social? The nature and controversies of measuring social return on investment (SROI).”; Alex Nicholls, “‘We do good things, don’t we?’: Blended Value Accounting in social entrepreneurship,” Accounting, organizations and society 34, no. 6-7 (2009).

6. Betsy Biemann et al., “A framework for approaches to SROI analysis,” Social Edge (2005); Maier et al., “SROI as a method for evaluation research: Understanding merits and limitations.”; Patrick W Ryan and Isaac Lyne, “Social enterprise and the measurement of social value: methodological issues with the calculation and application of the social return on investment,” Education, Knowledge & Economy 2, no. 3 (2008); Joseph J Cordes, “Using cost-benefit analysis and social return on investment to evaluate the impact of social enterprise: Promises, implementation, and limitations,” Evaluation and program planning 64 (2017).

7. Millar and Hall, “Social return on investment (SROI) and performance measurement: The opportunities and barriers for social enterprises in health and social care.”; Ryan and Lyne, “Social enterprise and the measurement of social value: methodological issues with the calculation and application of the social return on investment.”

8. Nicholls, “‘We do good things, don’t we?’: Blended Value Accounting in social entrepreneurship.”

9. Pratik Dattani, “Challenges and misconceptions in calculating SROI,” Spotlight Public Policy, Economic and Strategy Consulting, Londonavailable at: www. economicpolicy group. com/content/uploads/downloads/2012/10/EPG-Spotlight-Public-policy-Challenges-and-misconceptions-in-calculating-SROI-v1-1. pdf (2012); Pathik Pathak and Pratik Dattani, “Social return on investment: three technical challenges,” Social Enterprise Journal (2014); Ivy So and Alina Staskevicius, “Measuring the ‘impact’in impact investing,” Harvard Business School (2015).

10. Cordes, “Using cost-benefit analysis and social return on investment to evaluate the impact of social enterprise: Promises, implementation, and limitations.”

11. Cordes, “Using cost-benefit analysis and social return on investment to evaluate the impact of social enterprise: Promises, implementation, and limitations,” 100.

12. Cordes, “Using cost-benefit analysis and social return on investment to evaluate the impact of social enterprise: Promises, implementation, and limitations.”

13. Cordes, “Using cost-benefit analysis and social return on investment to evaluate the impact of social enterprise: Promises, implementation, and limitations.”

14. Susana Ferreira and Mirko Moro, “On the use of subjective well-being data for environmental valuation,” Environmental and Resource Economics 46, no. 3 (2010).